Companies like Amazon have used selection, pricing and convenience as levers to scale their businesses. Applying the same model to investment platforms will end up producing some adverse consequences.

I recently got my dad to switch his Mutual Fund investments from ICICI’s regular funds to Kuvera’s direct funds. Direct mutual fund investment companies are all the rage now. They offer a smoother user experience compared to old school distributors or banks, and more importantly, they save you a good deal of cash in the long term.

As I guided him over the phone to invest in one of the funds, I couldn’t help but appreciate how easy the process was thanks to the familiarity provided by the e-commerce platforms. The new investment platforms seem to follow a recognizable purchasing flow: you select a fund from a list of funds available using filters available, and add them to cart. Once you’ve added them to the cart, you can choose to either do a one time purchase or set up a monthly recurring investment schedule.

The ease provided by these platforms is remarkable. However, reflecting a little more throws up an interesting question: is making it easier to purchase mutual funds, especially using a eCommerce-like mechanism, necessarily a good thing? What could be the potential down sides to such a thing? Generally speaking, easing the process of buying complicated products online is rightly noted as a mark of progress. However, in this particular case, there are some potential downsides to making it easier to buy mutual funds, especially by following the practices used by e- commerce firms.

Unnecessarily large selection

There’s an inherent potency to the idea of choosing from a large selection. It feeds into our belief that we’re being more deliberate with our choices, and larger the catalog size, the more pronounced is this feeling of careful deliberation. Optimising on this feeling is one of the main promises of an eCommerce store, a store with a nearly infinite number of choices.

Surely there’s a reason why Boris Yeltsein, the ex-Soviet premier, when on a visit to the US was driven around to an American supermarket. This visit to the supermarketis said to have had more impact on him than his visit to the Johnson space center from where he had just returned. Being able to choose whatever we want from a multitude of options available in the aisles of supermarkets is a reflection of empowerment and freedom, something that wasn’t available to the ordinary Soviet citizens then.

While a large catalog may sometimes mean better selection when it comes to consumables, in the case of financial products, a larger selection adds to the noise, confusing the users into buying products that aren’t necessarily good for them. There is ample evidence to suggest that investors regularly make poor choices based on intuition, often unconsciously. A large selection catalog in most cases only exacerbates the situation ultimately incentivizing poor investment choices.

Loaded filters and tools

Tools like filters, sorting options and search boxes originally developed to buy clothes or electronic gadgets on online stores aren’t necessarily of much help in choosing the right financial products. This is because the filters and selection tools presume that users know what they’re looking for, an assumption that is almost definitely false in the case of people landing on the investment platforms to make the purchases.

This isn’t because choosing the right investment product requires some genius level math or some deep understanding of financial theories — in fact, the math rarely ever goes past high-school levels — but most of us are guided by behavioral biases that we’ve developed over the years from our experiences.

Take a very commonly prevalent behavioral bias called Anchoring: a term that is used to refer to the practice of how we often rely on unrelated figures and stories that we’ve recently heard or seen to evaluate upcoming decisions.

Do ‘popular’ investment choices necessarily make for right choices?

In my own experience, I’ve noticed often how users end up choosing or discarding mutual funds on the basis of their pre-conditioned attitudes towards the founders of the parent AMCs (Asset Management Companies) formed on the basis of online opinion pieces, and not on the basis of the performance of the fund in the question.

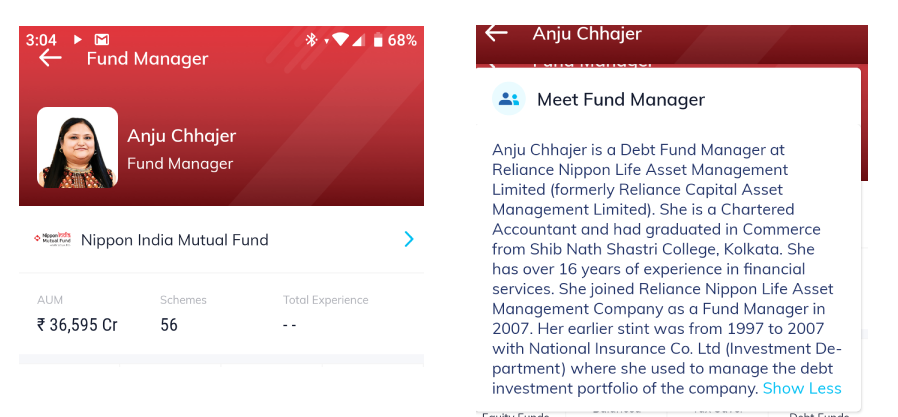

It is indeed a little disturbing to see a platform like PayTM money displaying the names and bios of the fund managers. While such information may be useful to a small minority of users, for most of the people on the platform, this additional information will only add to the noise already present and feed into the biases people may have about names, gender, college education, etc of these fund managers.

PayTM Money offers a bio of the fund manager. It is unclear as to whether this information can in any way help a user make better investment decisions.

Financial products, unlike many other consumables that one can purchase online, carry significant potential risks, and are only sorta-right for people buying them. That’s because one can never really be sure.

The most common misconception regarding these biases that we carry is that we’re somehow immune to them. Most of us are very convinced in the veracity of our own judgements. And the smarter we are, the more eloquent are the arguments we can make to ourselves defending our judgements. Despite our supposed omniscience, we very often end up making mistakes when it comes to purchasing investment plans.

Zero-Pricing

Besides offering a large selection, eCommerce stores like Amazon have served the end users well by decreasing the prices of the products by offering a competitive environment, and negotiating better deals on behalf of all the customers on the platform.

While there aren’t any such deals to be negotiated as far mutual fund investment products go, the new-age platforms seem to be capitalizing on a similar trend by choosing to sell Direct funds over Regular. That is, these platforms are choosing to not make any money from the purchases of their users. This isn’t very different from what has come to be the default method of operation by businesses online. Surely, in the case of B2C online commerce, not offering heavy discounts on services online is now seen as an aberration, unless it involves delivery of physical goods.

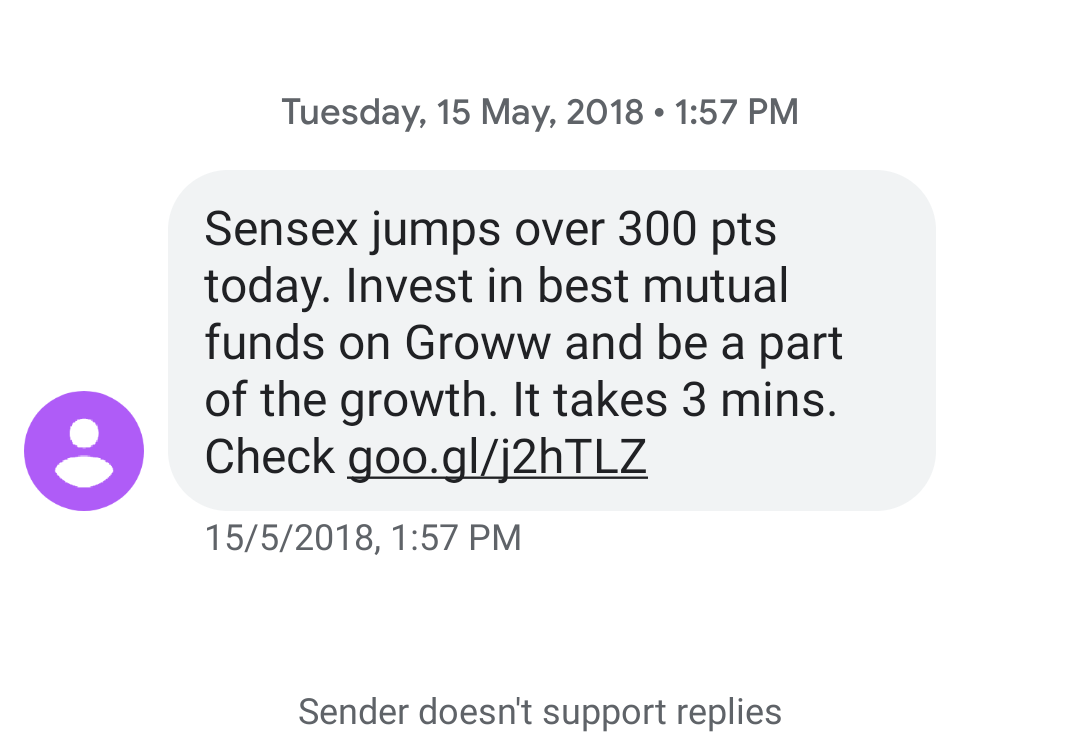

A promo SMS sent by Groww. Groww.in has (at least in the past) used market movements to encourage investments — much like how eCommerce stores have used discounts to drive up sales.

While zero-pricing the investment product certainly makes it cheaper for the users, and improves their yield on their investments, it comes with its own consequences. By choosing to offer their services for free, tech companies like Google and Facebook have had to develop a large-scale surveillance based business model. The model relies on extracting as much data about the users as possible, so that it can be used to create a more detailed profile of the user behaviors and preferences that can be consumed by advertisers to sell products to the user.

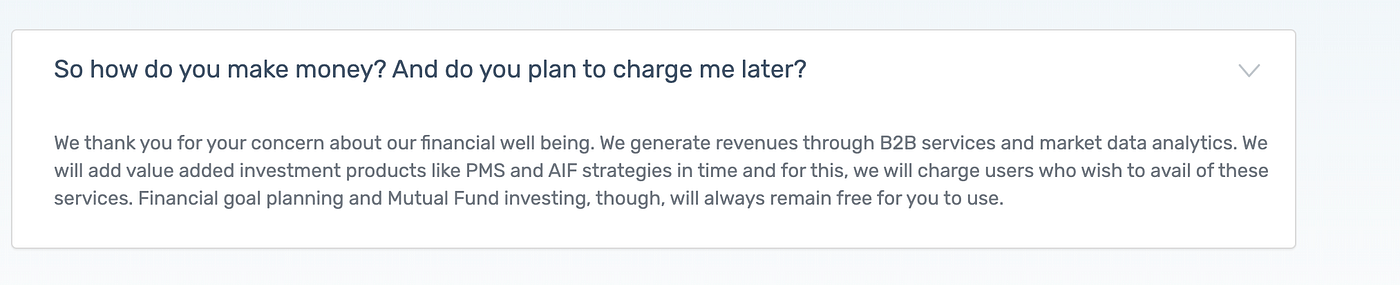

Here’s Kuvera’s answer to how it makes money

It isn’t clear as to how such a model could work in the case of investment products as yet. This is especially worrying since India doesn’t have strong data protection laws to safeguard the interests of the users. While some platforms are relying on abstract mental acrobatics to justify their claim that they will (in the future) figure it all out, others are choosing to rely on the old school method of making money from origination fees.

Kuvera, for example, cross-sells insurance products to the users who are investing in Mutual Funds through its platform — although this is done indirectly by forwarding the user to HDFC insurance site. The commissions from insurance products typically range in 25–40% of annual premiums. This is particularly striking since making money from insurance commissions stands in direct opposition to Kuvera’s claim of choosing to not profit from the investment choices behind the scenes.

Closing thoughts

Beyond some of the specific problems outlined above with following an eCommerce store like approach to building investment platforms, is an overarching belief propagated by these platforms that it is required of investors to spend a great deal of time and effort figuring out all the dials and levers to make the right investment decisions.

This method of active investing places an unnecessary burden on the users to build an understanding of the markets to invest safely. This is in direct opposition to the trends in developed markets like the US, where users are increasingly choosing to invest passively via index funds over actively managed funds. I understand that index funds in India may not compare well with Vanguard’s S&P 500. However, over the long term (especially after accounting for lower risk, turn over ratio, TERs), they can certainly produce good returns.

It’s still the proverbial “day zero” for these new age investment platforms, and as the Indian investor will evolve, things are bound to change. And there certainly is great value in the innovations by these platforms. However, it is important to understand the potential downsides of the disruption brought about by these companies and how it all connects to their business models.