Finding out the economics of UPI payments is like trying to play Pin the Tail on the Elephant with a blindfold on. Here’s what we know from the different NPCI circulars and media reports.

Update : I’ve written a sequel to this post based on the comments I received for this one.

The various tech blogs and newspapers can’t get seem to get enough of UPI-related news. Be it the recent news about Google pay making a boat load of money, or about how UPI can now be used to pay for Gondola rides you may take the next time you are in Venice, we’re constantly surrounded by news that celebrates the UPI network.

So innate is our belief in benefits of the UPI that we hardly ever question the fundamental economics of the network. It’s gotten to a point where I’m now scared to ask anyone about the economics of the UPI payments. I’m worried that I’ll be mocked at for having spent over two years in the Fintech space and still not knowing who makes how much.

Surely, if this fee-breakdown is common knowledge, one should expect to find it easily available online, like how one can find the interchange fees for Master card and Visa.

Sadly, this can’t be further from the truth. Working out the fee-structure of UPI payments requires one to stitch together and reconcile multiple circulars and press notes that the NPCI has put out over the years. The exercise is a lot like solving a haunted house mystery and requires the skills of an amateur detective from an Enid Blyton novel.

By not maintaining a straightforward and easy to understand settlements guide, the NPCI contributes towards creating an environment of mistrust and confusion.

Anyway, here’s the breakdown based on the sources I’ve found online. I invite any reader to write in to me if they know better. I’d like to think of this more as a public resource that can be updated as and when the changes happen.

Glossary:

NPCI: National Payments Corporation of India (NPCI), an umbrella organization that acts as the settlement agency for all UPI transactions.

PSP : A Payments Service Provider in the UPI ecosystem is a certified and trusted entity that users interact with for their payments. The PSP is essentially the technology provider. Could be the bank itself or it could be an entity which works with a bank/on behalf of the bank, like Google Pay, PhonePe, etc.

Acquirer bank: Also called the merchant bank, acquiring bank is the financial institution that maintains the merchant’s bank account.

Issuer Bank: An issuing bank, also known as issuer, is a bank or financial institution that offers UPI as a payment option to consumers. The issuing bank is responsible for providing the financial backing for the transactions made by its customers PSP.

Interchange fee: Interchange is a small fee paid by a merchant’s bank (acquirer) to a issuer bank to compensate the issuer for the value and benefits that merchants receive when they accept electronic payments.

MDR : Merchant Discount Rate is the cost paid by a merchant to a bank for accepting payment from their customers via UPI (or other payment methods). The merchant discount rate is expressed in percentage of the transaction amount.

For a detailed list see https://blog.50p.in/understanding-upi-b6a4b57ccdfb

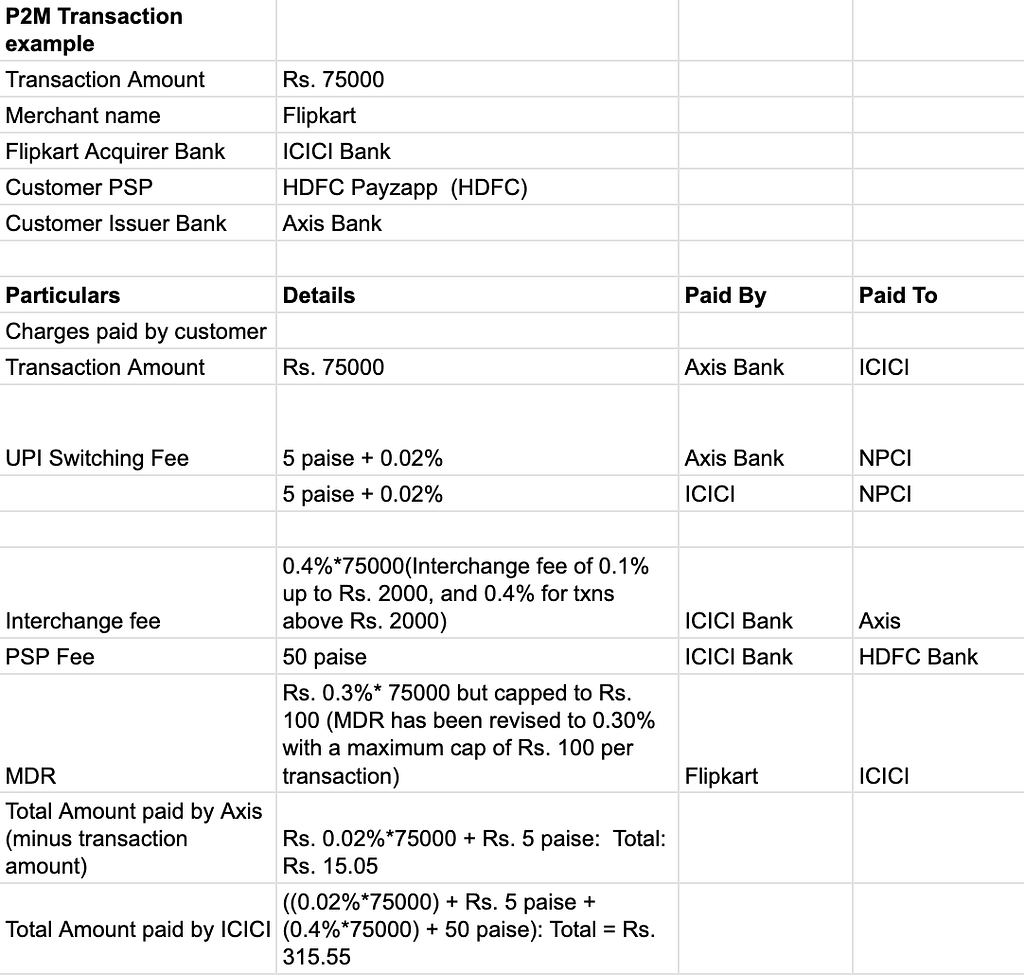

Person-to-Merchant (P2M) Transaction:

Here’s the breakdown for a P2M transaction considered between a user transacting with Flipkart using HDFC Payzapp app.

For details regarding the relevant circulars, please refer to this publicly available Google Sheet.

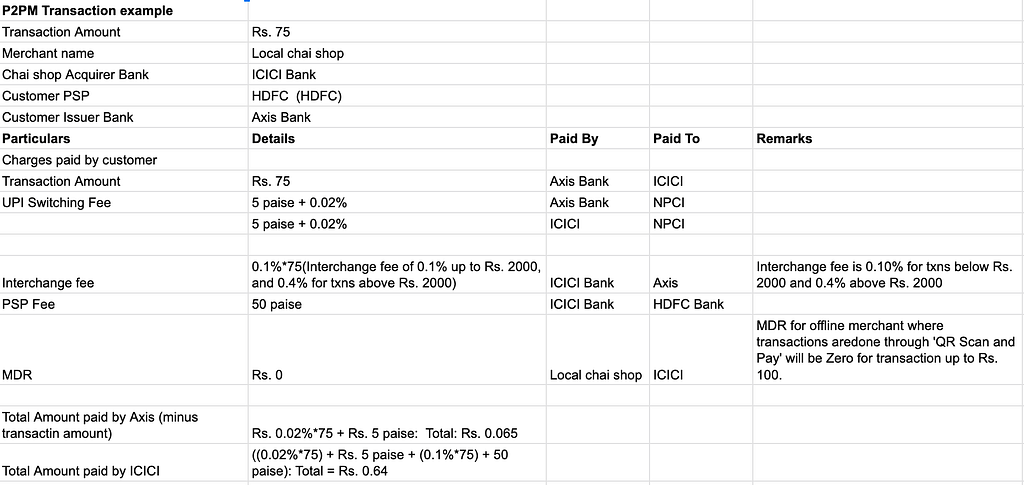

Person-to-Person-Merchant (P2PM )Transaction:

The NPCI introduced a new category of transactions,called P2PM transactions to categorize the transactions between persons and small businesses separately.

Below is a breakdown of a sample transaction between a user and a local chai shop. For details, refer to this Google sheet.

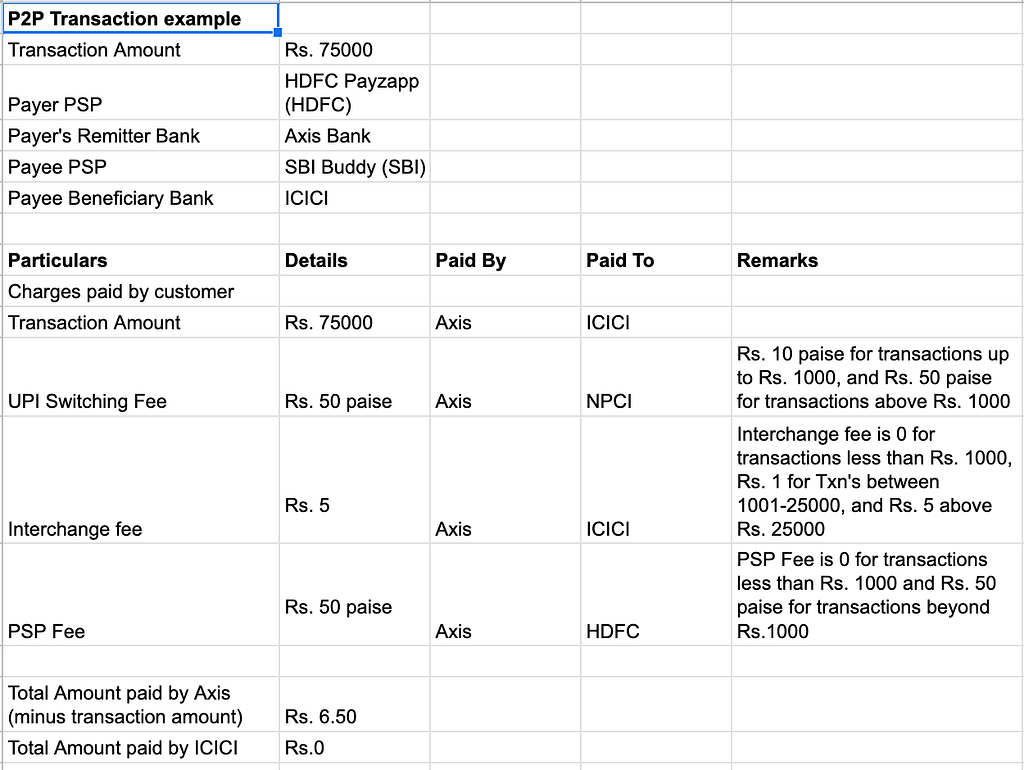

Person-to-Person (P2P) Transaction:

Here’s the breakdown for a P2P transaction considered between two users, one with an HDFC Payzapp app, and another with a SBI Buddy app.

For details regarding the relevant circulars, please refer to this publicly available Google Sheet.

Note: The older UPI settlement guide (not sure when this was published) mentions an IMPS switching fee in addition to the UPI switching fee. This fee of Rs. 50p is supposed to be paid by the remitter bank in the case of a p2p transaction, and by the issuer bank in the case of a p2m or p2pm transaction. However, I haven’t found any references to this fee in the circulars and media reports released over the last two years, so I’m not sure if this fee is applicable anymore.

Also, note that in the case of P2M transactions, with the MDRs being capped to 0.3%, it seems like the acquirer isn’t making any money after paying the interchange fee of 0.4% to the issuer. This doesn’t make any economic sense.

Brickbats, corrections and comments are welcome.

Check out the f ollow-up piece I wrote on this topic available here .